Momentum

1. INTRODUCTION

Momentum is a phenomenon that links asset’s return to its relative performance history. The basic mechanics of momentum is to rank assets by past returns relative to their peers, then take a long position in the past winners (portfolio of stocks with high past returns) and short the past losers (portfolio of stocks with low past returns). It is important to understand that the momentum is not the same as trend following, which primarily considers absolute performance, buying in the bull market and selling during the downswings, and hence being explicitly exposed to the market risk. In contrast to the trend following, momentum does not assume an explicit view on the market trend and defines ’winners’ and ’losers’ irrespective of whether the market is falling or growing. For example, during an extreme market-wide downturn the momentum’s winners are the securities that experience the lowest price decline relative to other securities over the same time period.

In their seminal paper Jegadeesh and Titman (1993) [1] show that buying winners (stocks with high returns in the past 6 months) and selling losers (stocks with low returns in the past 6 months) results in the average annualized excess return of 12.01% over the 6-month holding period (such strategy is also commonly denoted as UMD — ’up-minus-down’ and WML — ’winners-minus-losers’). Since then the momentum effect received a lot of attention from both academics and practitioners, making it one of the most studied and well-established phenomena in the empirical finance. Geczy and Samonov (2013) [2] assemble a dataset of the U.S. stocks, which spans the period from 1801 to 2012 (compare to the CRSP data, which is arguably the most popular U.S. stocks database for academic research and begins in 1926). In what they call ’the world’s longest backtest’, the authors document the profitability of momentum for 125 out-of-sample years, thus providing the evidence that momentum effect is robust to the data mining problem, and that it had been in the markets well before the very first academic research in financial economics appeared. Persistence of returns is not a unique feature of the U.S. stock market, over the past two decades the momentum effect has been found in foreign stocks, fixed income securities, commodities, currencies and global equity indices, moreover, a recent study by Asness et al. ( 2013) [3] discovers that UMD returns are strongly correlated across markets and different asset classes, suggesting presence of common global factors, which drive the premium.

Why does the momentum premium exist? The nature of the momentum effect is subject to debates in academic research. The views of the scientific community can be subdivided into two broad categories: behavioral- and rational-based explanations. The behavioral approach uses the well-documented human cognitive biases, such as investors’ overconfidence in their ability to evaluate securities; self-attribution bias (the investors put more trust in their private signals, than in the publicly available information); and the tendency to view events as representative or typical, ignoring the probabilities — all of these may result in under- and overreactions, thus leading to autocorrelation in asset returns. The rational asset pricing theories derive the short-term return continuation (momentum) and long-term return reversals (or equivalently value) from the firm’s production decisions and investment risk: the negative relation between investment and expected returns dates back to Cochrane, 1991 [4]; furthermore, Liu and Zhang (2008) [5] report that the growth rate of industrial production explains more than half of momentum profits. Vayanos and Woolley 2013 [6] suggest a very appealing rational explanation of persistent return patterns: the authors assume that investors delegate the management of their portfolios to financial institutions. Since the true skill of funds’ managers is unobservable to investors, the negative idiosyncratic shock to fundamental value of some assets leads to a negative update about managers’ abilities, in turn triggering outflows and consequent liquidations, which further depress prices. Given the realistic institutional constraints such as lock-up periods and decision lags, the price decreases gradually, resulting in momentum. At the same time, since assets are priced below their fundamental value, expected returns rise, giving way to reversal. Nevertheless, none of the theories are able to reproduce the observable variation in returns — the truth is, as always, somewhere in between: we do know that investors are not completely rational (think of herd behavior during the bubbles and crashes); but also that fundamentals are important (otherwise, nobody would care about insider trading).

2. PRACTICAL IMPLEMENTATION AND MOMENTUM MYTHS

As practitioners, we are not particularly interested in the exact mechanism behind momentum — both rational and behavioral theories justify the existence and, more importantly, persistence of the premium. We care more about different aspects of implementation of this strategy. These include, but are not limited to, risks and rewards of the strategy (for example, in terms of Sharpe ratio), trading costs associated with portfolio rebalancing , maximum drawdown, exposure to other factors such as liquidity and volatility, conditions under which one might expect a crash of the strategy, and so on. Not surprisingly, concerns about practical implementation of the momentum strategy have grown in number together with the amount of empirical evidence from academic research. Israel et al. (2014)[7] argue that some of these concerns have effectively become ’myths’. The authors identify 10 myths and refute them in a didactical way using the publicly available data from Kenneth French’s web page. Here we are going to discuss a couple of the myths, but we also strongly advise to read the original paper.

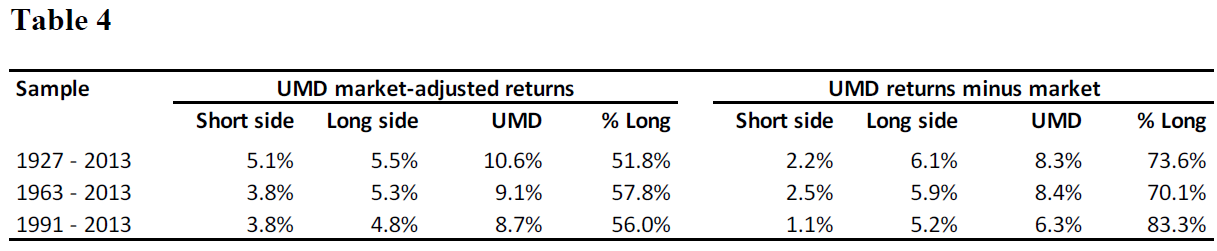

Myth #2: Momentum can be exploited on the short side only.

This statement claims that momentum gains come from the losers, so a typical investor who faces short selling constraints is unable to profit. The empirical evidence, however, is opposite. The table below summarizes the momentum’s performance for U.S. data. Historically, more than half of the UMD returns adjusted to market risk (or alphas) is earned by the winners. The returns of the momentum portfolio in excess of the market (the last four columns in the table) are actually larger for the ’up’ side—given that historically the market portfolio generates positive returns the long and short parts of UMD have different exposures to market risk. Imagine that we observe a bull market during the past year, then the ’up’ and ’down’ sides of the momentum portfolio include high- and low-beta stocks respectively, thus leaving the portfolio exposed to systematic downside risk.

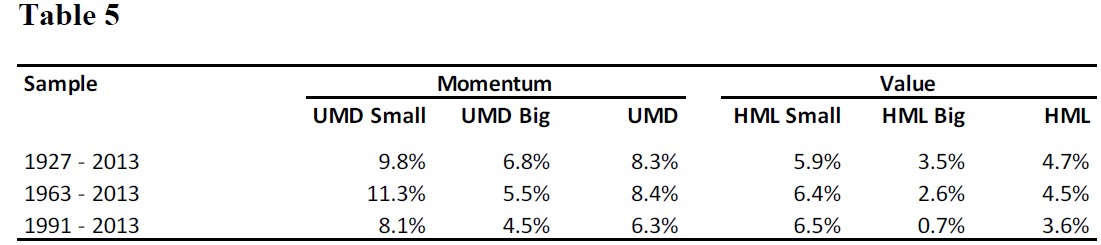

Myth #3: Momentum is much stronger among small caps.

Once again Israel et al. (2014)[7] employ Kenneth French’s data — for the whole sample the average annual returns for value and momentum portfolios that include only large cap stocks are 3.5% and 6.8% respectively. Furthermore, the value premium becomes insignificant once adjusted for market risk, while momentum does not. Actually, a single quotation from the original paper is enough for the Myth #3:

Putting it starkly: in-sample, out-of-sample, calculated in Greenwich Connecticut, Chicago, Boston, Palo Alto, Santa Monica, Austin, or in the library with a candlestick, wherever or however you want to look, along any dimension, those who make the claim that momentum fails for large caps, while being supporters of value investing, are not simply mistaken, they have it backwards.

We refer those readers who are interested in a more thorough overview of the roles of size and short selling in profitability of value and momentum to Israel & Moskowitz, (2013) [8]. This paper examines four international stock markets along with four additional asset classes (equity indices, commodities, currencies, and fixed income instruments) and documents dissipation of value premium with increasing size and no reliable effect of size on momentum returns.

3. RISKS OF MOMENTUM

For the U.S. stocks momentum demonstrates the highest historical Sharpe ratio of 0.5 in comparison with market (0.41), size (0.26), and value (0.39). However, the long-term gains are plagued by occasional crashes, hence implying a fat left tail of momentum returns’ distribution. Barroso and Santa-Clara (2012) [9] report UMD skewness of -2.47 and excess kurtosis of 18.24, along with losses of -91.59% in two months in 1932 and -73.42% in three months in 2009. These two crashes were caused by the rapid rebound of market after long-lasting declines —during the long bear market the short side of UMD portfolio gets exposure to the market risk by accumulating high-beta assets, thus resulting in huge losses in case of a sudden market upswing. The effect is less pronounced for an opposite situation of long part of UMD and previous positive market trend. This evidence suggests a need for careful management of momentum’s risks. Daniel and Moskowitz (2013) [10] and Barroso and Santa-Clara (2012) [9] propose dynamic momentum strategies, which use conditional variance forecasts in order to determine optimal exposure to UMD factor and optimal weights for UMD constituents. Both approaches result in more than doubled Sharpe ratios and significantly reduced skewness of momentum returns.

4. TIME SERIES MOMENTUM

Time series (or absolute) momentum refers to persistent trends in prices of individual securities. Interestingly, the theoretical models that predict momentum usually analyze a single risky asset, so, ironically, we have explanations for trends and not for the heterogeneity of asset-specific returns. The time series momentum is just as universal as its cross-sectional counterpart: Moskowitz et al. , (2012) [11] find the past 12 month performance to be a significant predictor of future 1 to 12 months returns for equity indices, commodities, currencies, and sovereign bonds. The time series momentum is also found to fully explain the cross-sectional momentum for all asset classes except the equity indices, while having small loadings to other standard factors. Nevertheless, the risks of the strategy still remain unexplored.

5. SUMMARY

Although we still have no theoretical explanation, which grasps all of the observed facts and justifies the existence of momentum, the empirical evidence of returns’ persistence is overwhelming for different markets and assets classes. What is important for a practitioner, is that the momentum profits are still there and are robust to transaction costs, size, short selling constraints, taxation, etc. What is even more important, is that, despite the attractive Sharpe ratio and high excess returns, the momentum returns’ distribution tends to have the fat left tail and the strategy is subject to occasional significant losses (the risk comes from the conditional exposure to market), so implementation in practice demands thorough risk management.

References

- Returns to buying winners and selling losers: Implications for stock market efficiency,

, The Journal of Finance, Volume 48, Number 1, p.65–91, (1993)

- 212 Years of Price Momentum (The World’s Longest Backtest: 1801–2012),

, Working Paper, (2013)

- Value and Momentum Everywhere,

, The Journal of Finance, Volume 68, Number 3, p.929–985, (2013)

- Production-based asset pricing and the link between stock returns and economic fluctuations,

, The Journal of Finance, Volume 46, Number 1, p.209–237, (1991)

- Momentum profits, factor pricing, and macroeconomic risk,

, Review of Financial Studies, Volume 21, Number 6, p.2417–2448, (2008)

- An institutional theory of momentum and reversal,

, Review of Financial Studies, p.hht014, (2013)

- Fact, Fiction and Momentum Investing,

, Working Paper, (2014)

- The role of shorting, firm size, and time on market anomalies,

, Journal of Financial Economics, Volume 108, Number 2, p.275–301, (2013)

- Managing the Risk of Momentum,

, Working Paper, (2012)

- Momentum Crashes,

, Working Paper, (2013)

- Time series momentum,

, Journal of Financial Economics, Volume 104, Number 2, p.228–250, (2012)

- Log in to post comments